Krugman blogs:

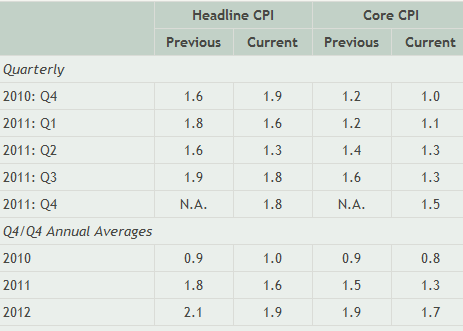

As Catherine Rampell points out, this is the lowest level of core inflation ever.

But I have a question here: why do economic forecasters keep predicting a near-time rise in core inflation, even though they are also predicting high unemployment? The Survey of Professional Forecasters now predicts average unemployment of 8.7 percent in 2012, which would seem to be a recipe for continuing disinflation and quite possibly deflation; but the same forecasters predict a noticeable rise in core inflation over the next two years:

Meanwhile in Europe, the debt crisis resurfaces. Dean Baker blogs:I don’t really understand this, except as a fundamental unwillingness to face up to the Nipponization of the US economy.

Ireland is in the headlines these days as its government struggles with insolvency. Remarkably, none of the news stories remember to point out that Ireland was a model of fiscal responsibility in the years leading up to its current disaster. Not only did it balance its budget, Ireland ran large budget surpluses in the 5 years preceding its collapse in 2008. Its peak surplus in 2006 was 2.9 percent of GDP, the equivalent of a surplus of roughly $420 billion in the United States.

Like the deficit hawks in the United States, Ireland's political leaders ignored the country's massive housing bubble, the collapse of which sank its economy. It is interesting to note that, while Ireland's background to the deficit crisis is generally ignored, news reports on Greece's financial difficulties routinely referred to its large budget deficits in the years leading up to the crisis.And yet here we are in the US talking about deficits and the Catfood Commission.

No comments:

Post a Comment