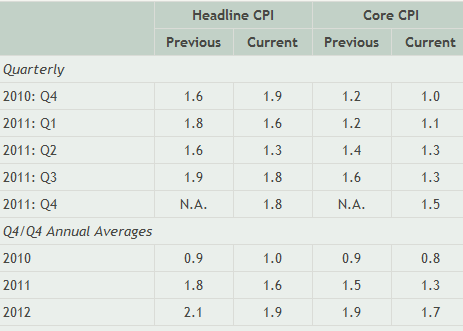

The new thing for me is the realization - reading Waldman - that we will be in a liquidity trap for a long time. Atlanta's Lockhart says QE is not "QE infinity."

Yesterday Steve Williamson blogged:

Yesterday Steve Williamson blogged:

The quantity of reserves held by US financial institutions is now approaching $1.6 trillion, and the Fed has promised to increase that stock by $85 billion per month for the indefinite future. Thus, it seems safe to say that the Fed will be working within a monetary regime with a large quantity of excess reserves for a very long time.All Your Base Are Belong To Us, Continued (Still Wonkish) by Krugman

Krugman "And I think he’s implying that there’s really no difference between 2(b) and 3." 3 is what MMTers argue something Krugman has discussed before.

Waldman "But Waldman definitely does not at all believe that 2(b) and (3) are equivalent when the interest rate is positive." So he's not a subscriber to MMT?

At Economic View, Sadowski links to "the Money Illusion":

Currency matters even with IOR by Scott Sumner

Which I can't make sense of. As I understand it, there are three schools of demand management: the Modern Monetary Theoryist (MMTers, far left), the Market Monetarists (rightwing) and the mainstream DeLong-Krugman-Thoma axis to which I subscribe.

A link history of this discussion:

Debt in a Time of Zero by Krugman

It’s true that printing money isn’t at all inflationary under current conditions— that is, with the economy depressed and interest rates up against the zero lower bound. But eventually these conditions will end. At that point, to prevent a sharp rise in inflation the Fed will want to pull back much of the monetary base it created in response to the crisis, which means selling off the Federal debt it bought. So even though right now that debt is just a claim by one more or less governmental agency on another governmental agency, it will eventually turn into debt held by the public.

We are living in weird economic times, where many of the usual rules don’t apply and there are big free lunches to be had. But not everything is a free lunch, even now. Sorry.Which led to Ip's blogpost which linked to the above:

Platinomics by Greg Ip

But the politics are utterly different. We have a central bank to separate fiscal from monetary policy. The Fed implements QE when it has decided that’s the best way to carry out its monetary policy objectives. Buying a coin solely to finance the deficit is monetizing the debt, precisely the sort of thing central bank independence was meant to prevent. How could any Federal Reserve chairman justify cooperating in such a scheme, in particular since the Fed would be taking the White House’s side in a fight with Congress over a matter of dubious legality?

Yes, the Fed has sacrificed its independence for the sake of the national interest before, such as maintaining a ceiling on Treasury yields between 1942 and 1951; but that was (initially) in wartime, and it eventually led to inflation. Would avoiding the debt ceiling be important enough to compromise the Fed's independence? Perhaps not in this one case; but it would set a precedent future presidents will happily exploit and feed the perception that America’s economic institutions are in terminal decline. America has had debt ceiling crises before (in 1957, 1985, 1996 and 2011) and survived; are the unknown risks of the platinum coin option obviously preferable to the known risks of hitting the debt ceiling?Duy linked to both Krugman and Ip:

On The Disruptiveness of the Platinum Coin by Tim Duy

Carrying the argument further, the illusion of a difference between cash and debt at the zero bound is counterproductive because it prevents the full application of fiscal policy. Fears about the magnitude of the government debt prevent sufficient fiscal policy, but such fears are not rational if debt and cash are perfect substitutes. If cash and debt are the same, the fiscal authority should prefer to issue cash if debt concerns create a false barrier to fiscal policy. Still, I would argue that this is best done in cooperation with the monetary authority. Note that this is not really a new idea, as then Governor Ben Bernanke drew a similar conclusion with regards to Japan:

However, besides possibly inconsistent application of fiscal stimulus, another reason for weak fiscal effects in Japan may be the well-publicized size of the government debt...In addition to making policymakers more reluctant to use expansionary fiscal policies in the first place, Japan's large national debt may dilute the effect of fiscal policies in those instances when they are used....My thesis here is that cooperation between the monetary and fiscal authorities in Japan could help solve the problems that each policymaker faces on its own. Consider for example a tax cut for households and businesses that is explicitly coupled with incremental BOJ purchases of government debt--so that the tax cut is in effect financed by money creation.

And then we come to the platinum coin, which threatened to expose the illusion that cash and debt are different at the zero bound....

...Waldman links to Duy and Ip:

Ultimately, I don't believe deficit spending should be directly monetized as I believe that Paul Krugman is correct - at some point in the future, the US economy will hopefully exit the zero bound, and at that point cash and government debt will not longer be perfect substitutes. Note that Greg Ip disagreed with this point:

I disagree. The Fed does not have to sell its bonds, or the $1 trillion coin, to control inflation (though it may do so anyway). It only needs to retain control of interest rates, and that does not depend on the size of its balance sheet.

There’s no such thing as base money anymore by Steve Randy WaldmanKrugman responds

All Our Base Are Belong To Us (Wonkish) by KrugmanWaldman responds

Do we ever rise from the floor? by Steve Randy Waldmanand then Krugman responds again (see above) and Waldman responds again (see above)

Update:

Tim Duy has another post:

My takeaway from Waldman is that under some institutional structures, there is little difference between platinum coins and government debt (or because we have debt we have a particular institutional structure?) In effect, the the zero-bound issue and platinum coin debate have forced us to think down paths that blur the lines between fiscal and monetary policy. The longer we are in at the zero-bound, the more we will challenge the existing status-quo.

Alternatively, this can also be simply a misunderstanding on Krugman's part if he believes that Waldman is saying that we can use platinum coins to literally monetize deficit spending with neither budgetary nor inflationary implications. I don't think Waldman is thinking this, and if he is, then I think he would be wrong.And commenter RebelEconomist (from the UK) at Waldman's latest:

What a lot of fuss about nothing! Americans might save themselves much confusion if they paid more attention to practices in other countries. Well before the financial crisis and QE, the Bank of England switched to paying interest on reserves to make the demand for reserves more elastic and hence make moneymarket interest rates, through which the BoE regulated its monetary stance, less volatile. Provided that the interest rate paid on reserves is a bit less than low credit risk private sector debt, the banks will still hold reserves primarily as a settlement asset, but simply hold more reserves. On May 18 2006, the day the new regime was introduced, reserves held by British banks rose about twenty fold, a demand met by the BoE, without any disturbance to inflation, sterling exchange rates or government debt markets. I explain the reasoning in more detail in this old post of mine:

http://reservedplace.blogspot.co.uk/2009/04/easing-understanding.html

(especially paragraphs 20-24). I suspect that the Fed always wanted to introduce such a system themselves, but found it difficult to get past populist congressmen whining about giving money away to banks, and now they have it, they are going to hang onto it for operational reasons long after they cease paying interest on reserves for QE purposes!Commenter Tom Hinkey at interfluidity:

I think that it is unlikely that the Fed will continue the setting floor rate by paying IOR for political reasons similar to the reason that the platinum coin was smothered in the crib. It gives the game away and threatens the illusion that government finance is like firm or household finance under the current monetary regime. This is not an operational requirement since there is no operational reason for government not to fund itself directly. The illusion that government needs to be funded from revenue or borrowing from the private sector is created by political means, that is legislation, regulation, and interpretation. There is serious speculation that the central bankers’ club nixed the platinum coin gambit for this reason, and I would not be surprised to see TPTB nix payment of IOR when it no longer suits their purposes.Another Updated(!)

Once you turn base money into short-term debt, can you go back? by Izabella Kaminska