Saturday, December 18, 2010

Explaining the Crisis with Dogma by Joe Nocera

I hope this is an eye opener for young people with functioning brain cells who are trying to figure out what's going on instead of just focusing on getting by.

I like Nocera and agree with his openly stated views but it wasn't very smart of him to bash Hewlett Packard's board in his column while his wife was working as a lawyer against those same people.

And yet he was very smart to team up with Bethany McLean and I am looking forward to reading their book.

I always cut people who I admire a lot of slack. (Although I never cut Clinton much slack, I do cut Obama some). They're human.

Krugman once consulted for Enron, but he learned from his mistake - although I'm not clear on the details - and will write:

I hope this is an eye opener for young people with functioning brain cells who are trying to figure out what's going on instead of just focusing on getting by.

I like Nocera and agree with his openly stated views but it wasn't very smart of him to bash Hewlett Packard's board in his column while his wife was working as a lawyer against those same people.

And yet he was very smart to team up with Bethany McLean and I am looking forward to reading their book.

I always cut people who I admire a lot of slack. (Although I never cut Clinton much slack, I do cut Obama some). They're human.

Krugman once consulted for Enron, but he learned from his mistake - although I'm not clear on the details - and will write:

Or consider the California electricity crisis of 2001-2002. Years after we actually had tapes in which Enron traders could be heard telling power plants to shut down, news reports continued to repeat the conservative line that it was all about excessive regulation that wouldn’t let the power companies build capacity -- with no mention at all of the market manipulation.In the same blog post, a good reference:

Put it this way: I’ve been rereading George Orwell’s Looking Back at the Spanish War, and it feels familiar.

Friday, December 17, 2010

Wall Street Whitewash by Krugman

Take a Load Off Fannie: Why won't the GOP's financial-crisis report follow the money? by Bethany McLean

Take a Load Off Fannie: Why won't the GOP's financial-crisis report follow the money? by Bethany McLean

Thursday, December 16, 2010

Leonhardt on legal opposition to health care law

"We are against forcing all citizens, regardless of need, into a compulsory government program," said one prominent critic of the new health care law. It is socialized medicine, he argued. If it stands, he said, "one of these days, you and I are going to spend our sunset years telling our children, and our children’s children, what it once was like in America when men were free."

The health care law in question was Medicare, and the critic was Ronald Reagan. He made the leap from actor to political activist, almost 50 years ago, in part by opposing government-run health insurance for the elderly.

Today, the supposed threat to free enterprise is a law that’s broader, if less radical, than Medicare: the bill Congress passed this year to create a system of privately run health insurance for everyone. On Monday, a federal judge ruled part of the law to be unconstitutional, and the Supreme Court will probably need to settle the matter in the end.

Tuesday, December 14, 2010

What Progressives Don’t Understand About Obama by Ishmael Reed

Deeper Looks at the Crisis of ’08 and the Oval Office by Michiko Kakutani

Deeper Looks at the Crisis of ’08 and the Oval Office by Michiko Kakutani

Echoing what Jonathan Alter wrote about the president in his recent book, "The Promise," Mr. Wolffe writes that "there were few around him who thought health care was the right way for Obama to define his first year," especially given the state of the economy. But the president pushed ahead anyway: in part, Mr. Wolffe suggests, because of memories of his mother’s worries about medical insurance in the months before her death from cancer; in part because it was a priority for the first lady; in part because he aspired to be a great, history-making president and liked to "take on the toughest political challenges he could find"Reading David Plouffe's book, I learned that heath care reform was the number one priority for Democratic party primary voters.

Monday, December 13, 2010

Saturday, December 11, 2010

Krugman on Charles Stross and the amoral corporation

One thing I like about blogs is when writers I admire discuss other writers from other fields who they admire. And one of the things I like about Krugman and DeLong is that they're polymaths and not soley focused on economics. Krugman blogs:

Hitchens writes about the Tea Party.

Nixon resigned when I was almost 4 years old. Recent released tapes of years in Presidency reveal his prejudice against Jews, blacks, Irish, and Italians. No doubt the Republican elite knew of it and probably shared his hate for the most part. Same thing with the voters and many Democrats.

And almost 40 years later we have a black President. That's progress.

One thing I like about blogs is when writers I admire discuss other writers from other fields who they admire. And one of the things I like about Krugman and DeLong is that they're polymaths and not soley focused on economics. Krugman blogs:

If you ask how it’s possible that a handful of bad actors can get their way so often, the answer has to be, wasn’t it ever thus? What we call civilization has usually been a form of kleptocracy, varying mainly in its efficiency (the Romans were no nicer than the barbarians, just more orderly). Yes, we’ve had a few generations of government somewhat of, by, for the people in some places -- but that’s an outlier in the broader sweep of things.

So never mind the hive-minds; good old greed still rules.Yes but there is progress. Often the kleptocrats are helped by red herrings and distractions like racism and clerical demogoguery.

Hitchens writes about the Tea Party.

Nixon resigned when I was almost 4 years old. Recent released tapes of years in Presidency reveal his prejudice against Jews, blacks, Irish, and Italians. No doubt the Republican elite knew of it and probably shared his hate for the most part. Same thing with the voters and many Democrats.

And almost 40 years later we have a black President. That's progress.

Thursday, December 09, 2010

"We need a tow, not a jump-start."

Obama referenced Mark Zandi in defending the stimulus component of the tax cut deal.

Krugman responds that we're in a process of deleveraging at his blog here and here.

I disagree with Krugman's criticisms of Obama, but Krugman could be right if the engine of the private sector doesn't get going. My view is that he's wrong to personalize the issues when it comes to Obama by saying stuff like Obama isn't a fighter. He isn't tough enough? The first black President? The man has no fear. Obama, Axelrod, and Plouffe took on the Clinton machine in the Democratic primary and dealt with their hard ball tactics with "dirt off the shoulder."

It gets me down when he links to Digby or DeLong links to Jane Hamsher or Atrios.

Obama referenced Mark Zandi in defending the stimulus component of the tax cut deal.

Krugman responds that we're in a process of deleveraging at his blog here and here.

I disagree with Krugman's criticisms of Obama, but Krugman could be right if the engine of the private sector doesn't get going. My view is that he's wrong to personalize the issues when it comes to Obama by saying stuff like Obama isn't a fighter. He isn't tough enough? The first black President? The man has no fear. Obama, Axelrod, and Plouffe took on the Clinton machine in the Democratic primary and dealt with their hard ball tactics with "dirt off the shoulder."

It gets me down when he links to Digby or DeLong links to Jane Hamsher or Atrios.

Wednesday, December 08, 2010

G.E. and JPMorgan Got Lots of Fed Help in ’08 by Sewell Chan and Jo Craven McGinty

Also in the New York Times Magazine, Daniel Bergner on John Pendergrast:

The two companies received help even as their chief executives, Jeffrey R. Immelt of G.E. and Jamie Dimon of JPMorgan, sat on the nine-member board of the Federal Reserve Bank of New York.

Neither executive was involved in creating the emergency programs, which were approved by the Fed’s board of governors in Washington. Both companies also disclosed that they were among scores of institutions that received support from the Fed. Nevertheless, some policy experts expressed discomfort with the situation.

"In my view, it is an obvious conflict of interest for C.E.O.’s of banks and large corporations who serve on the Fed’s board of directors to have received cheap loans from the Fed," Senator Bernard Sanders, a Vermont independent who wrote the legal provision requiring the Fed to make the disclosures, said in a statement on Sunday.

...

Goldman, previously an investment bank, became a Fed-regulated bank holding company during the crisis. It tapped the Fed program to help investment banks 52 times, owing $18 billion to the Fed at one point -- receiving far greater support than JPMorgan.

The chairman of the New York Fed at the time, Stephen Friedman, was a Goldman director and former chairman of Goldman. The Fed granted Mr. Friedman a waiver so he could continue serving as chairman of the New York Fed.

While awaiting the waiver, Mr. Friedman bought shares of Goldman around the time the bank received Fed support. After The Wall Street Journal reported on the purchases, Mr. Friedman stepped down, saying the Fed "does not need this distraction." The New York Fed’s top lawyer said at the time that Mr. Friedman "did not violate any Federal Reserve statute, rule or policy."

Mr. Friedman’s successor as chairman of the New York Fed was Denis M. Hughes, president of the New York State A.F.L.-C.I.O. Fed observers say it is unlikely that a former banker will serve as the agency’s chairman any time soon.Jamie Dimon: America’s Least-Hated Banker by Roger Lowenstein in the New York Times Magazine:

TARP became a symbol of bailout policy gone awry. Actually, the program has succeeded for banks and, thus far, for the government. Taxpayers earned $795 million on the J. P. Morgan stake. Dimon is upset that people think he was bailed out. But there is at least some truth to the view of Christina Romer, a former economist for President Obama, who notes that Dimon "was part of the system that gave rise to the crisis. He certainly benefited. If the system went south, he’d have gone south with everybody else."Christina Romer on uncertainty in the economy

The deepest and most destructive uncertainty we face centers on the overall health of the economy and its prospects for growth. Unlike other postwar recessions that were caused by tight monetary policy and high interest rates, the recent downturn resulted from the bursting of a housing bubble and a financial crisis. Because we are in largely uncharted territory, figuring out how and when the economy will recover is much harder than usual.I think we know what to do, it's Republican opposition that is the problem (see for example the lunacy Rep. Mike Pence of Indiana and Senator Corker of Tennesse about how the Fed shouldn't concern itself about unemployment. And so Republican Bernanke has to go on 60 Minutes to defend the Fed.) Othewise I agree strongly with Romer's Op-ed.

Also in the New York Times Magazine, Daniel Bergner on John Pendergrast:

"I do human rights the way I played basketball," John Prendergast said. We were sitting in the outdoor restaurant of an unfinished hotel in Juba, a boomtown of mud and shanties beside the White Nile in southern Sudan. It’s a restaurant where the South’s liberation leaders tend to gather, and these days they are in a buoyant mood. They have traded their fatigues for dress shirts and suits. A half-century of civil war seems to be culminating in independence. If a referendum on Jan. 9 goes as expected, the map of Africa will be redrawn " with a new nation around the size of Texas. But for the moment, Prendergast, who is America’s most influential activist in Africa’s most troubled regions and who huddled on a White House patio with President Barack Obama a few days earlier, talked about basketball guards.

...

One way to understand Prendergast’s influence, suggested Samantha Power, who is the National Security Council’s senior director for multilateral affairs and human rights and who counts Prendergast among her close friends, is not to see Obama as lacking a sense of urgency on Sudan were it not for Prendergast’s recent activism, but rather to view the president as long-engaged on Sudan partly because of the highly successful advocacy movement Prendergast helped to start several years ago around the crisis in Darfur. And now, she continued, on North-South peace, Prendergast is "creating a political space; he’s putting political wind in the sails of people who care about this issue: the president, Denis" -- she nodded toward McDonough, the deputy national security adviser -- "me. He’s elevated Sudan to Himalayan proportions on the mattering map in Washington." While this may be an overstatement, Prendergast has surely helped to pull an expanse of scrub and swamp, and the people who live upon it, into American sightlines.(emphasis added)

Tuesday, December 07, 2010

Krugman on Poland and the euro

Good piece in the Times about the advantages Poland is deriving from not having adopted the euro (yet):

The floating zloty, which has fallen about 18 percent against the euro since early 2009, acted as a pressure release valve, helping to keep Polish products competitive on world markets and insulating Poland from the effects of the sovereign debt crisis.

Poland has proved itself to be Europe’s most dogged economy during the last two years. It was the only member of the European Union to avoid recession, soldiering on even after a plane crash in April killed much of the political elite, including the president and the central bank governor. No banks needed to be rescued.You want to think about just how hard it would be to cut wages 18 percent, as opposed to achieving it automatically via depreciation.

Monday, December 06, 2010

Movie about the Clash in the works

Just the other a day an employee at the local used book store in my neighborhood was shocked when Mick Jones and Paul Simonon entered the store, browsed and asked if they had a certain book. They were playing with Gorillaz who were performing at a local music venue that night.

Just the other a day an employee at the local used book store in my neighborhood was shocked when Mick Jones and Paul Simonon entered the store, browsed and asked if they had a certain book. They were playing with Gorillaz who were performing at a local music venue that night.

Saturday, December 04, 2010

Coen Brothers' True Grit remake coming soon

With a sly hipness that is the trademark of Joel and Ethan Coen, a billboard just outside the Melrose Avenue gate at Paramount Pictures promotes their next film, "True Grit," with a promise: "Retribution. This Christmas."It's funny but is it "hipness"?

But other film devotees were less charmed, particularly when they viewed "True Grit" through the filter of Vietnam-era politics and Wayne’s conservative principles -- which he had said were illustrated by a scene in which Cogburn shoots a rat after demonstrating the futility of trying to treat it under due process of law. (The new film has no such moment.)

Writing in The New Yorker, Penelope Gilliatt complained of the movie’s "very right-wing and authoritarian tang." She was particularly put off by the frontier stoicism, which she described as "near-Fascist admiration for a simplified physical endurance of pain"

In The New Republic, Stanley Kaufman said of Mr. Portis’s novel, "Although it was short it was overlong by about a third." The film’s director, Henry Hathaway, he described as "an old workhorse" who "hasn’t had a new idea since the beginning of his career"

President Richard M. Nixon, for whom Wayne had campaigned, apparently felt otherwise, if a snippet of conversation caught by his Oval Office taping system in February 1971 is any measure. Greg Cumming, an archivist with the Nixon Library, said that the audio quality of the tape was bad, but that he could make out Nixon’s discussing "True Grit: with his chief of staff, H. R. Haldeman. They talk of someone’s having gone "out in a blaze of glory," according to Mr. Cumming.

Of course, Wayne went on to make about 10 or so more films, including the 1975 sequel "Rooster Cogburn," before his death in 1979.

The Coens said they only dimly recalled having seen the earlier movie when they were young, and they did not watch it in preparing their own. "We didn’t do our homework," Ethan Coen said.

Joel Coen said they were drawn to the underlying book a few years ago after he had "re-read it out loud to my kid."1969 trailer:

Friday, December 03, 2010

Sewell Chan on the Fed data dump

From December 2007 to October 2008, the Fed opened swap lines with foreign central banks, allowing them to temporarily trade their currencies for dollars to relieve pressures in their financial markets.

The European Central Bank drew the most heavily on these currency arrangements, the records show, but nine other central banks also made use of them: Australia, Denmark, England, Japan, Mexico, Norway, South Korea, Sweden and Switzerland.

Monday, November 29, 2010

The Spanish Prisoner by Krugman

But problems were developing under the surface. During the boom, prices and wages rose more rapidly in Spain than in the rest of Europe, helping to feed a large trade deficit. And when the bubble burst, Spanish industry was left with costs that made it uncompetitive with other nations.

Now what? If Spain still had its own currency, like the United States -- or like Britain, which shares some of the same characteristics -- it could have let that currency fall, making its industry competitive again. But with Spain on the euro, that option isn’t available. Instead, Spain must achieve "internal devaluation": it must cut wages and prices until its costs are back in line with its neighbors.

And internal devaluation is an ugly affair. For one thing, it’s slow: it normally take years of high unemployment to push wages down. Beyond that, falling wages mean falling incomes, while debt stays the same. So internal devaluation worsens the private sector’s debt problems.

What all this means for Spain is very poor economic prospects over the next few years. America’s recovery has been disappointing, especially in terms of jobs -- but at least we’ve seen some growth, with real G.D.P. more or less back to its pre-crisis peak, and we can reasonably expect future growth to help bring our deficit under control. Spain, on the other hand, hasn’t recovered at all. And the lack of recovery translates into fears about Spain’s fiscal future.

Friday, November 26, 2010

Wednesday, November 24, 2010

Lands of Ice and Ire by Krugman

Iceland versus Ireland; heterodox versus orthodox.

Iceland versus Ireland; heterodox versus orthodox.

What’s going on here? In a nutshell, Ireland has been orthodox and responsible -- guaranteeing all debts, engaging in savage austerity to try to pay for the cost of those guarantees, and, of course, staying on the euro. Iceland has been heterodox: capital controls, large devaluation, and a lot of debt restructuring -- notice that wonderful line from the IMF, above, about how "private sector bankruptcies have led to a marked decline in external debt". Bankrupting yourself to recovery! Seriously.

And guess what: heterodoxy is working a whole lot better than orthodoxy.

Tuesday, November 23, 2010

Monday, November 22, 2010

Dean Baker: Robert Samuelson Does the Big Lie, Big Time

Competent budget analysts know that the long-term budget problem is a health care cost problem. If U.S. per person health care costs were comparable to those in any other wealthy country, we would be looking at huge projected surpluses not deficits. Because health care costs are rising rapidly in the private sector, it means that the public sector programs that pay for these benefits (most important Medicare and Medicaid) also have rapidly rising costs.

If Medicare and Medicaid are lumped together with any other programs then the combination of Medicare, Medicaid, and the other program will be the cause of the deficit. For example, the categories of Medicare, Medicaid, and foreign aid explain the vast majority of the projected increase in the deficit over the next quarter century. Similarly, the combination of Medicare, Medicaid, and school lunch programs also explains the vast majority of the projected increase in the deficit over the next quarter century.

Robert Samuelson throws in Social Security as the third program so that he can tell readers:

"America's budget problem boils down to a simple question: How much will we let programs for the elderly displace other government functions."

Social Security does not in any honest way since it is fully financed over the period in question by the designated Social Security tax. But Samuelson does not feel bound by such details.

Of course there are easy ways to prevent health care costs from bankrupting the country, most obviously by taking advantage of the lower cost health care available in other countries. But, Samuelson never discusses such possibilities, focusing exclusively on cutting benefits on which the vast majority of retirees depend.via Yglesias, Joe Klein on the Pain Caucus's focus on "fiscal resposibility":

here is, for example, Glenn Hubbard, who was featured on the New York Times op-ed page recently in defense of the deficit commission, describing the problem this way: "We have designed entitlements for a welfare state we cannot afford." This is the same Glenn Hubbard who served as George W. Bush’s chief economic adviser when Dick Cheney was saying that "Reagan proved deficits don’t matter." One imagines that if Hubbard was so concerned about deficits, he might have resigned in protest from an Administration dedicated to creating them. But, no, he’s here to speak truth to the powerless -- to the middle-class folks whose major asset, their home, was trashed by financial speculators, thereby wrecking their retirement plans and creating the consumer implosion we’re now suffering. Hubbard is telling them they now have to take yet another hit, on their old-age pensions and health insurance, for the greater good.

Sunday, November 21, 2010

Professor predicts Obama will win in 2012 because economy will be better.

Paul Barrett reviews "All the Devils Are Here: The Hidden History of the Financial Crisis." by Bethany McLean and Joe Nocera.

Barrett writes

Bernanke and Krugman point to the global savings glut rather than the Fed's policy of keeping rates low after the dot-com crash of 2000 as the source of the housing bubble which took on a life its own once it had momentum.

His model forecasts real annualized growth in gross domestic product of 3.69 percent for the first three quarters of 2012. A survey of leading economists by Blue Chip Economic Indicators shows an average forecast of 3.2 percent growth in real G.D.P. in 2012, while the Congressional Budget Office estimates 3.4 percent. Plug either of these estimates into his election algorithm and the result is the same: President Obama wins.He believes the Fed will keep policy stimulative.

Paul Barrett reviews "All the Devils Are Here: The Hidden History of the Financial Crisis." by Bethany McLean and Joe Nocera.

Others have illuminated facets of the crisis in more depth. John Cassidy’s "How Markets Fail" explained the economic history and theory with greater sophistication. Gillian Tett’s "Fool’s Gold" offered a journey into one investment bank, J. P. Morgan, and a close look at how it helped create a financial instrument, the credit derivative, that amplified risk rather than minimizing it. "In Fed We Trust," by David Wessel, took the reader behind the scenes in Washington, where politicians and regulators missed all the warning signs. For their part, McLean and Nocera concentrate on the basics and bring them together in brisk, well-organized chapters.I've read Cassidy's book and Wessel's book, but need to get Tett's.

Barrett writes

Another public quarrel McLean and Nocera bring into focus is the esoteric debate about Federal Reserve monetary policy. Ben S. Bernanke, the chairman of the Federal Reserve, has pushed interest rates practically to zero to try to stimulate growth and reduce an unemployment rate that currently hovers near 10 percent. Dissenters from this policy, like Thomas M. Hoenig, the president of the Kansas City Federal Reserve Bank, warn that Bernanke is repeating the mistake of his predecessor, Greenspan, who employed similar measures to combat the recession that followed the dot-com crash of 2000.There are two different issues about Greenspan. His approach to regulation and his approach to interest rates. Hoenig and Barrett erroneously conflate the two.

Bernanke and Krugman point to the global savings glut rather than the Fed's policy of keeping rates low after the dot-com crash of 2000 as the source of the housing bubble which took on a life its own once it had momentum.

Saturday, November 20, 2010

Depression Economics in a Nutshell by Brad DeLong

Second is excess demand for liquid cash money.

Historically, we have had three types of excess demand for finance that have produced big downturns in economies.In 2002 there was an excess demand for bonds and so logically there was less demand for currently produced goods and services. Brad doesn't say it, but that was in the aftermath of the Tech Bubble crash. He writes that in 2008 there wasn't excess demand for bonds because they are still cheap. They would be expensive if there was an increased demand.

Second is excess demand for liquid cash money.

It is possible to tell when there is monetarist downturn: since everybody is trying to build up their stocks of liquid cash money, everybody is selling their other financial assets and thus their prices--stocks, bonds, whatever--and all their prices are low. That is not the kind of downturn we have today: today the prices of some financial assets--the liabilities of credit-worthy governments, for example--are very high.Third is an excess demand for safety after the housing bubble popped and the ensuing panic.

We conclude that the excess demand in financial markets right now on the part of investors is an excess demand for safety: for high quality AAA-rated assets for people that hold in their portfolios. Prices of risky financial assets are low--there is no excess demand for them. Prices of safe financial assets are high--there is an excess demand for them.

Thus businesses and households have cut back on their spending on currently-produced goods and services as they all have concluded: "We don’t have enough safe assets in our portfolios. We need to stop spending so much until we build up our holdings of safe assets to a higher level." And the fact that they cannot do so because there is a shortage of safe assets in the economy is what is keeping us wedged in this current situation of high unemployment and low capacity utilization.

Where did this excess demand for safe assets come from?

It came as a consequence of the deregulation of finance and of the securitization of mortgages, from the housing bubble and the crash, from the fact that then it turned out that investment banks that had created brand new derivative securities based on mortgages had not originated-and-distributed them but had, to a remarkable and astonishing degree, originated and kept them. They were supposed to sell off all the pieces o[f] real estate risk in small bundles to savers all over the world. They did not.

Thursday, November 18, 2010

Federal Reserve Bank defends QE2. by Sewell Chan

The Republicans who signed the letter were the Senate minority leader, Mitch McConnell of Kentucky; Senator Jon Kyl of Arizona; Representative John A. Boehner of Ohio, who is in line to become the House speaker in January; and Representative Eric Cantor of Virginia, the No. 2 House Republican. They emphasized that the Fed should be insulated from political pressure but also said the central bank "should be open to receiving input and data from a wide range of sources."

However, the letter was more moderate in tone than recent complaints voiced by other Republican critics, like Representatives Mike Pence of Indiana, the chairman of the House Republican Conference, and Kevin Brady of Texas, who is in line to lead a subcommittee on trade.

By contrast, in the Fed’s corner on Wednesday was Thomas J. Donohue, president of the United States Chamber of Commerce, which poured money into the midterm campaigns to defeat Democrats.

"The Fed has over many, many, many years been particularly helpful to this government and to this country in dealing with financial crises, and by the way, they always make money on it," Mr. Donohue told reporters, referring to the fact that the Fed each year turns over to the government the profit it makes as a byproduct of its investments. "We’re hopeful that the Fed’s judgments turn out to be very positive for job creation and economic expansion."

Mr. Donohue suggested that some of the criticism of Mr. Bernanke had gone too far, praising Mr. Bernanke as a scholar of the Depression and saying, "We must maintain the independence of the Fed and be very, very careful not to louse that up on Capitol Hill:"

The Beatings Will Continue Until Morale Improves

Irish Officials Acknowledge Need for Aid in Debt Crisis.

Ireland: a Textbook Example of the Dangers of Balanced Budgets and Fiscal Responsibility by Dean Baker

OECD sees global recovery slowing

Irish Officials Acknowledge Need for Aid in Debt Crisis.

Ireland: a Textbook Example of the Dangers of Balanced Budgets and Fiscal Responsibility by Dean Baker

OECD sees global recovery slowing

January 7th panel in Denver at the AEA Annual Meeting

Panel Moderator: John Quiggin (University of Queensland, Australia)

Brad DeLong (University of California-Berkeley) Lessons for Keynesians

Tyler Cowen (George Mason University) Lessons for Libertarians

Scott Sumner (Bentley University) A defense of the Efficent Markets Hypothesis

James K. Galbraith (University of Texas-Austin) Mainstream economics after the crisis

Wednesday, November 17, 2010

Wikipedia entry on "duel" and dueling.

Isaac Asimov relates a joke in his Treasury of Humor (1971) that claims that Otto von Bismarck challenged Rudolf Virchow to a duel. As the challenged party had the choice of weapons, Virchow chose two sausages, one of which had been infected with cholera. Bismarck is said to have called off the duel at once.

One Way to Trim Deficit: Cultivate Growth by David Leonhardt

Krugman blogs:

Krugman blogs:

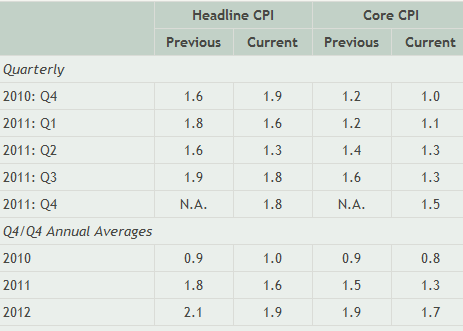

As Catherine Rampell points out, this is the lowest level of core inflation ever.

But I have a question here: why do economic forecasters keep predicting a near-time rise in core inflation, even though they are also predicting high unemployment? The Survey of Professional Forecasters now predicts average unemployment of 8.7 percent in 2012, which would seem to be a recipe for continuing disinflation and quite possibly deflation; but the same forecasters predict a noticeable rise in core inflation over the next two years:

Meanwhile in Europe, the debt crisis resurfaces. Dean Baker blogs:I don’t really understand this, except as a fundamental unwillingness to face up to the Nipponization of the US economy.

Ireland is in the headlines these days as its government struggles with insolvency. Remarkably, none of the news stories remember to point out that Ireland was a model of fiscal responsibility in the years leading up to its current disaster. Not only did it balance its budget, Ireland ran large budget surpluses in the 5 years preceding its collapse in 2008. Its peak surplus in 2006 was 2.9 percent of GDP, the equivalent of a surplus of roughly $420 billion in the United States.

Like the deficit hawks in the United States, Ireland's political leaders ignored the country's massive housing bubble, the collapse of which sank its economy. It is interesting to note that, while Ireland's background to the deficit crisis is generally ignored, news reports on Greece's financial difficulties routinely referred to its large budget deficits in the years leading up to the crisis.And yet here we are in the US talking about deficits and the Catfood Commission.

Tuesday, November 16, 2010

Philly Fed revises downwards. I bet the economy does better than this but it's just a hunch.

(via DeLong, via Atrios)

Under Attack, Fed Officials Defend Buying of Bonds by Sewell Chan

Bernanke and the Fed have been attacked by China, Germany etc., Greenspan and conservative letter writing economists.

Yglesias directs us to this by Greg Mankiw. He didn't sign the letter, nor did Mark Zandi. Both have gone up in my book. Greenspan seems to have reverted to form after admitting he was wrong about self-regulating banks.

Tim Duy writes:

(via Mark Thoma)Bottom Line: In general, the retail sales report was good news, as it is another indicator that drives a stake into the heart of the double-dip story. But keep in mind that the data continues to illustrate the good cop, bad cop conflict in the economy. Policymakers should be concerned about the distance between new trends and old, lest they risk falling into the trap of diminished expectations, believing that 9% unemployment should be the new normal. Market participants, however, may simply be content with confirmation that the foundation for ongoing corporate revenue growth remains secure.

Krugman responds to fellow columnist David Brooks:

Brooks is a member of my "rogues gallery."

So David Brooks claims that

The economic approach embraced by the most prominent liberals over the past few years is mostly mechanical. The economy is treated like a big machine; the people in it like rational, utility maximizing cogs. The performance of the economic machine can be predicted with quantitative macroeconomic models.I protest, on several grounds.

First, it’s conservative economists who insist that people are always rational and utility-maximizing; liberal economists are the ones willing to invoke bounded rationality, animal spirits, etc.. The whole salt-water fresh-water split was about which you were going to believe: the assumption of perfect maximization, or your own lying eyes. And the Keynesians were the ones who preferred to believe their eyes.

Second, David would have us believe that the Obama people were misled by their excessive faith in models. But we actually know what happened when the stimulus was being discussed: the modelers, who said that we needed something much bigger, were dismissed in favor of gut feelings about market psychology.

David Brooks: Math is Hard, Just Give Money to Rich People by Dean BakerThe truth is that we would have been much better off if Obama et al had relied on old-fashioned hydraulic Keynesianism.

Brooks is a member of my "rogues gallery."

Friday, November 12, 2010

Wednesday, November 10, 2010

Krugman on the Catfood Commission.

Update: It’s here. And it really is that bad. The idea that co-chairs of a commission whose charge is fiscal sustainability should take it upon themselves to (a) declare that federal revenue must not exceed 21 percent of GDP -- that’s right, putting a cap on receipts and (b) call for reducing the top rate from 35 to 23 is just awesome.This is how history will judge Obama. I can't believe he will go there. If so he will really demoralize his base. Hopefully the economy will recover by 2012 and the independents will come back as the Republicans implode. But Boehner seem smarter than Gringrich.

Monday, November 08, 2010

Yglesias asks:

Now that the campaign’s been over for a while can we all step back and ponder how nutty it was for Meg Whitman to spend $140 million on a failed bid to become Governor of California?

Gretchen Morgenson writes about an analyst who saw the housing bubble and is now seeing the economy turning the corner by August 2011 based on his analysis of small business.

Saturday, November 06, 2010

Krugman writes about how sticky prices are the prices to worry about, not volatile price.

He blogs about it here too.

He blogs about it here too.

Greg Ip on Sebastian Mallaby - that great fawner of hedge fund managers:

Like Mr Mallaby I regret the retreat from financial globalisation, but if it substitutes for naked protectionism, I can live with it. One thing other countries should not do is ask America to leave unused one of the few effective policy tools it has left to stimulate the domestic economy. The world needs higher unemployment and deflation in America like a hole in the head.(via DeLong)

Friday, November 05, 2010

I was talked into seeing the new Clint Eastwood/Matt Damon movie Hereafter* even though communing with the dead isn't my cup of tea. (However I do love the Mexican holiday Day of the Dead which sounds like a zombie horror flick**) I do like Eastwood and Damon however and was willing to give it a go even if burblings from the beyond bore me.

Damon's character is psychic and can communicate with people's dead loved ones, but it is upsetting for him. To calm himself down at night he listens to audio recordings of Charles Dickens' works, which I thought was interesting. There can be something soothing to an articulate old-timey British accent for an American for some reason.

The video is a recording of the new Chicago-based band the Secret Colours whose influences are Blur, The Jesus and Mary Chain, Stone Roses, Charlatans UK and the '67 London UFO scene. I'm looking forward to seeing them in concert.

---------------------

* Saddest movie ever made is Atom Egoyan's The Sweet Hereafter. I like to give "hippie peaceniks" a hard time but this scene about hippies is great.

**Maybe because there is one. AMC's new program The Walking Dead is pretty good zombie fun.

Wednesday, November 03, 2010

Wednesday, October 27, 2010

Friday, October 22, 2010

Michael Tomansky on Juan Williams.

Because what sort of non-conservative - one perceives Williams to be some degree of liberal; he'd probably protest that he's just a reporter; in either case, he's not a conservative - agreed to be an in-house flunky at Fox? I'm sure they offered him nice money, and money is money, and I can't say with certainty that I'd have turned it down if Rupert had waved it under my nose.

But if you're any kind of liberal at all, even in the softest and most non-political possible sense, it's basically an indefensible thing to do. Fox News wants liberalism to perish from the face of the earth. Going on their air on a regular basis and lending your name and reputation to their ideological razzle-dazzle is like agreeing to be the regular kulak guest columnist at Pravda in 1929. For "balance".I disagree. That analogy is wrong. Plus Williams was better than Colmes. Colmes is/was horrible.

Krugman on Austerity in the UK

Indeed, there has been a noticeable change in the rhetoric of the government of Prime Minister David Cameron over the past few weeks -- a shift from hope to fear. In his speech announcing the budget plan, George Osborne, the chancellor of the Exchequer, seemed to have given up on the confidence fairy -- that is, on claims that the plan would have positive effects on employment and growth.

Instead, it was all about the apocalypse looming if Britain failed to go down this route. Never mind that British debt as a percentage of national income is actually below its historical average; never mind that British interest rates stayed low even as the nation’s budget deficit soared, reflecting the belief of investors that the country can and will get its finances under control. Britain, declared Mr. Osborne, was on the "brink of bankruptcy"

What happens now? Maybe Britain will get lucky, and something will come along to rescue the economy. But the best guess is that Britain in 2011 will look like Britain in 1931, or the United States in 1937, or Japan in 1997. That is, premature fiscal austerity will lead to a renewed economic slump. As always, those who refuse to learn from the past are doomed to repeat it.

Thursday, October 21, 2010

.svg.png)

Dean Baker's entire post on the "currency wars" is excellent, so I'll repost the entired thing.

The NYT had a piece on the recent decline in the value of the dollar and effort by other countries to offset its impact. The article noted in particular developing country efforts to reduce capital inflows that are raising the value of their currency.

It would have been worth noting that in standard economic theory, developing countries are supposed to be borrowers. The logic is that capital is relatively scarce in the developing countries, which means that it gets a higher return. Capital therefore should flow from relatively to slow growing rich countries to more rapidly growing developing countries.

This was the direction of flows until the East Asian financial crisis in 1997. The harsh conditions that the IMF imposed on the East Asian countries led developing countries throughout the world to focus on building up reserves so that they would not have to deal with the IMF. This reversal coincided with the "high dollar" policy touted by then Treasury Secretary Robert Rubin. It helped to lay the basis for the imbalances associated with the stock and housing bubbles.

To a large extent, the decline in the value of the dollar would effectively reverse the distortions to the world economy resulting from the IMF-Rubin policy of the late 90s. It is also worth noting the recent decline in the dollar is largely just reversing its run-up as a result of the financial crisis in 2008. Money flowed into the U.S. as a safe haven, pushing the dollar well above its pre-crisis levels. It is now falling back toward the level it was at before the crisis.What would you call the reasonable reaction of China and others to the harsh conditions imposed by the IMF in the wake of the 1997 crisis? It would be the opposite of morale hazard. Once can be too indulgent and too harsh or strict.

This New York Times piece argues that England's current austerity measures are partly due to memories of the IMF bailing them out in the 1970s.

Tuesday, October 19, 2010

Of Turning Japanese

A scary chart from Mary Daly, vice president of the Federal Reserve Bank of San Francisco. (via Krugman, via Mark Thoma)

Brad DeLong doesn't believe the QE2 will be enough. (sorry no link) Dean Baker argues that we are already - as they used to say in Vietnam - in the shit. (sorry no link) If we cross past zero, it won't mark anything new just that we are continuing our descent of disinflation. The point when we entered a Keynesian situation is where we crossed the rubicon.

What is needed is a larger QE and more fiscal stimulus.

Democrats, the election, the stimulus and Keynes by Sewell Chan

But that seems unlikely, as long as the recovery plods along slowly. "It would be a mistake to attribute the distancing from Obama’s stimulus entirely to political caution or opportunism," said Robert S. Weisbrot, a historian at Colby College. "As much as those factors may be important, it is dismaying how little evidence there is to show for it. Maybe we need even more, but surely $800 billion should have counted for something"

Krugman blogs

During the pre-crisis period, spending grew slightly faster than GDP --that’s Medicare plus the Bush wars -- while revenue grew more slowly, presumably reflecting tax cuts.

What happened after the crisis? Spending continued to grow at roughly the same rate -- a bulge in safety net programs, offset by budget-slashing at the state and local level. GDP stalled -- which is why the ratio of spending to GDP rose. And revenue plunged, leading to big deficits.

What the usually good Sewell Chan fails to report is that the much of the stimulus was ineffective tax cuts and that much of the rest was canceled out or negated by the anti-stimulus of the 50 state governments and the stalling of GDP growth. Currently the economy is growing too slow to create enough jobs and aggregate demand which is why we'll see more action from the Fed.But I’m sure that the usual suspects will find ways to keep believing that it’s all about runaway spending.

Tuesday, October 12, 2010

Obama Fed nominee Peter Diamond wins Noble Prize for Economics

It is believed that Senate Republicans will ultimately not try a filibuster to block Professor Diamond now that he has been renominated. (His nomination was said to have been initially blocked in retaliation for a refusal by Democrats to give a full 14-year term to Randall S. Kroszner, who served on the Fed board from 2006 to 2009.)

If confirmed, Professor Diamond would complete a 14-year term that expires on Feb. 1, 2014.

Saturday, October 09, 2010

.svg.png)

The usually well-informed Ezra Klein says something odd this morning:I think it's an open question. Bernanke said the same thing in his June testimony. My guess is that it's all of the above: the stimulus and inventory effects are fading and the European sovereign debt crisis happened. I'm not sure but I would guess that it pushed up the dollar and made businesses and consumers more cautious. No doubt it helped the austerians rhetorically. They could now point to Greece as example of what could happen to a country that wracks up too much debt.

In 2007 and 2008 we had a major financial crisis. That led to a wrenching recession. But what killed the recovery was the European debt crisis. It was proof that there wasn’t just one risk that the system hadn’t properly accounted for, but many risks. And in a fragile global economy, the impact of any negative event was going to be magnified.I don’t know where Ezra got that, but it’s just not right. It’s not as if we had a solid recovery, then Greece came along. We never had the basics for self-sustaining recovery in place: aside from the stimulus and inventory bounce, demand remained weak. And financial jitters from the eurozone crisis had nothing to do with the US slowdown; growth is flagging because both the stimulus and inventory effects are fading.

Update: Ezra Klein repsonds

But a lot of the economists, business types and policymakers I've talked to have pinned the European debt crisis as a moment when whatever confidence various players had in the recovery collapsed. It was a whole new world moment: We hadn't just gone through one horrible, unlikely event and now we were recovering, and people should plan for a slow return to normal. The debt crisis was emphasized that there are a lot of risks out there and the world economy is vulnerable to them. The danger for businesses looking to invest wasn't just that demand could come back slowly but that everything could totally fall apart.

My guess is Krugman would dismiss that as rationalization. If government had responded to the crisis correctly and the economy was gaining more jobs and people were buying more things, businesses would be investing to meet the demand. And I agree with that. But in the absence of the correct government response, there's certainly a range of possible ways the private sector could've reacted, and I think it's plausible that their extreme caution is partly a response to seeing the world economy as vulnerable to all sorts of unpredictable shocks, which is leading them to wait for much more solid evidence of recovery than might otherwise be the case.

On the other hand, Krugman has a Nobel, and I, well, don't.Along with the deleveraging in the economy and not enough aggregate demand, I would guess another problem is "over"-demand for safe assets because people are nervous, in part because of the lack of aggregate demand. The European sovereign debt crisis would have added to this nervousness, unlike, say, Obama's tax and regulatory policies. But as Klein says, I don't have a Noble either.

Thursday, October 07, 2010

From Dsquared:

Day of the TriffinsVia Wikiepdia:

I am mildly surprised that Paul Krugman hasn't used this as a title for a blog post about the US$/yuan exchange rate yet. I donate it as open source to the community.

That is all.

Triffin dilemma(via DeLong)

The Day of the Triffids

Mario Vargas Llosa has won the Nobel Prize for Literature.

He wrote The Feast of the Goat (La fiesta del chivo), a political thriller, which was published in 2000 (and in English in 2001). It was based on the dictatorship of Rafael Trujillo, who governed the Dominican Republic from 1930 until his assassination in 1961.

He wrote The Feast of the Goat (La fiesta del chivo), a political thriller, which was published in 2000 (and in English in 2001). It was based on the dictatorship of Rafael Trujillo, who governed the Dominican Republic from 1930 until his assassination in 1961.

Competitive Nonappreciation*

Geithner Call for Global Cooperation on Currency by Sewell Chan

Financial Shock and Awe by Barry Eichengreen

(via Mark Thoma and Brad DeLong)

* what often happens in marriage. Spouses compete on who can not appreciate the other the most. (sad trombone sound - wah wah)

Geithner Call for Global Cooperation on Currency by Sewell Chan

As finance officials from around the world gather here this weekend for the annual meetings of the I.M.F. and the World Bank, American officials are concerned that the degree of cooperation in the recent financial crisis is eroding. In particular, the Obama administration is looking to the I.M.F. to help bring about what months of negotiations have failed to achieve: greater exchange-rate flexibility by China.I'm pretty sure the competitive devaluations of the 1930s helped ameliorate the Depression.

Instead of the "competitive devaluation" of the 1930s, which exacerbated the Depression, the world faces a threat of "competitive nonappreciation," Mr. Geithner said, citing a term coined by Edwin M. Truman, a former official at the Treasury and the Federal Reserve.

That was a reference not only to China but also Japan and Brazil, which have taken steps recently to prevent their currencies from rising in value.

Financial Shock and Awe by Barry Eichengreen

(via Mark Thoma and Brad DeLong)

First, it is a misunderstanding to believe that the policies pursued by the BOJ, the Fed, and the Bank of England come at one another's expense. What we are seeing, in all three cases, is not exchange rate manipulation but what is known as quantitative easing, actual or incipient. The evolution of BOJ policy makes this clear. What two weeks ago started as a modest foreign exchange market intervention has now turned into an explicit program of purchasing 5 trillion yen of Japanese treasury bonds and bills, commercial paper, exchange traded funds, and real estate securities. The Bank of England has made no bones about its continued commitment to quantitative easing. The Fed is moving slowly, slowly in the same direction.Eichengreen sees the Fed employing "shock and awe" methods in the data, but wishes they would be more explicit. (Krugman notes that the markets appear to believe in QE2) He hopes China sees reason as well, but I doubt they will.

This, of course, is precisely what is needed in a world where deflation has again become a problem and fiscal policy, for better or worse, is off the table. It is not a "beggar thy neighbor race to the bottom." If anything it is a race to the top.

The Fed needs to stop dithering and make precise the extent of the quantitative easing it intends. Uncertainty about whether it will move in increments or adopt a policy of shock and awe is contributing to the erratic behavior of the dollar exchange rate.Eichengreen believes the European Central Bank is still fighting the last war, but will eventually come around.

Not only would more clarity help that exchange rate settle down, but in addition it would make it easier for other central banks to calibrate their own policies. In particular, a Fed policy of shock and awe which, recent data increasingly suggest, is what is called for will make it easier for China to calibrate an appropriate response. With China experiencing inflation rather than deflation, looser credit conditions are the opposite of what it needs. Its challenge is to continue to modestly cool off its economy. Delinking from Fed policy by delinking from the dollar is the obvious way of achieving this result.

The ECB, for its part, needs to start planning for the next battle instead of incessantly fighting the last. If it ends up with an exchange rate of $1.50 to the euro, the European economy tanks, and in the absence of growth the Greek, Irish, and other fiscal austerity programs will collapse. It will only have itself to blame.--------------------------------------------

Here's a prediction: Contrary to what the markets currently assume, the ECB will eventually join the quantitative easing bandwagon. The only question is whether by the time it does it will already be too late.

* what often happens in marriage. Spouses compete on who can not appreciate the other the most. (sad trombone sound - wah wah)

Wednesday, October 06, 2010

Krugman on Quantatative Easing: the Sequel:

So I didn’t and don’t think that we can count on monetary policy to do the job; blithely declaring that the Fed should target nominal GDP misses the difficulties. And that means we need fiscal policy.On China, Krugman notes Martin Wolf agrees with him but favors Daniel Gros's reciprocity on capital controls. Krugman doesn't see how you could do capital controls on one country.

Of course, at this point, with the loss of political will, it looks as if we’re going to see an attempt to do the trick with quantitative easing alone. I hope it works, but I wouldn’t bet on it.

I'd support trying Gros's idea - which is what China is doing to us - Krugman's tariffs and the Eichengreen/Yglesias combo devaluations. Try all three and once we're at full employment, back off again.

Tuesday, October 05, 2010

How to Get Ahead

(or Lawyer Up!)

[spoiler alert]

I saw "The Social Network" and found it entertaining and thought-provoking, as everyone has been saying. The actors were all good, especially Jesse Eisenberg, Andrew Garfield, and Justin Timberlake.

Basically, Jesse Eisenberg plays Mark Zuckerberg whose Harvard friend Eduardo Saverin, played by Andrew Garfield, gives him a computer algorithm that allows him to create a software program Facemash which gets him noticed by the Winklevi twins and their friend Divya Narendra, who hire him to program their dating program. He uses some of the ideas from their dating program, his Facemash program, and some start-up money from Saverin to start his Facebook site.The ever-more-popular website gets noticed by Justin Timberlake's Sean Parker who lures Zuckerberg out to Silicon Valley and connects him with venture capitalists. And the website becomes more popular. Keep in mind, though, that Saverin did give him the original algorithm and the original start-up money.

Some random thoughts: Facebook caught on because of the aesthetic design which lacked advertisements and the relationship status on people's profiles. It caught on despite the existence of similar websites like MySpace and Friendster, and became a success because of the various efforts of Mark Zuckerberg and his business partners. No one can take that away from them, but the movie does portray Zuckerberg screwing over his friend and business partner Saverin. Saverin was duped into signing away his stake in the company, so I guess the morale of the story is one should have one's own lawyers look over these sorts of contracts even if it involves a contract with a "friend."

The characters seem real because they have both likable and unlikable qualities. They're complicated. Garfield's Saverin was the most sympathetic in the film, although you could see how Zuckerberg could be annoyed by his frequent mentions of his father. Also, the movie seems to say Saverin's focus on advertising was the wrong way to go for Facebook and Zuckerberg was correct to follow the business advice of Timberlake's Parker who among other things connected Zuckerberg with venture capitalists and suggested he change the name of the site from The Facebook to just Facebook. Parker and Zuckerberg also had an endearing desire to "stick it to the Man," or at least to stick to people who were patronizing and disrespectful to them. Maybe it's the adolescent boy in me who finds that trait appealing, because the movie also shows how that trait can lead people astray. Also, Parker and Zuckerberg obviously have other psychological "issues" for all of their business savvy.

The movie posits the possibility that Zuckerberg set up his businesses partners Saverin - via the cruelty to a chicken - and Parker - via a police bust - which really would have been Machiavellian, but ends up suggesting that he probably didn't. One of his lawyers* advises him to settle a lawsuit because a jury might think he had indeed set up his business partners to get them out of the way, because of some unethical and malicious behavior Harvard had disciplined him for before Facebook was up and running.

In my previous post, I had a quote where David Carr and producer Scott Rudin want to divide the views on Zuckerberg into Tragic or Heroic. Why not be dialectical and describe him as both? Or can the Tragic encompass the Heroic? Zuckerberg can be a visionary, perfectionist, tough, driven workaholic who got lucky and still be a flawed, unethical asshole.

Update: In his article on how the movie ignores the importance of "network neutrality," Lawrence Lessig writes

Lessig happens to be a professor at Harvard Law School and the director of the Edmond J. Safra Foundation Center for Ethics. He's right about net neutrality and the chair-making analogy, but I don't see what's ethical about misleading your business partner about what's in the contract he was signing. Saverin wouldn't have signed it had he understood what he was signing. In Lessig's view it's acceptable to screw over a sucker? I realize a lot of businesses operate this way - not to mention whole industries like Wall Street - but is it moral?

Is that good business ethics to lie to your business partners? Evidently it's good business. Marx was right about how capitalism reduces everything to the "cash nexus" which is why America is such a litigious society. At one point the old money Winklevi twins are at odds about suing Zuckerberg over intellectual property theft. One twin doesn't want to sue because "that's not how things are done at Harvard" which is a nod at the old aristocratic traditions and codes of honor, a vestigial feudal frame of reference. The twins' partner Divya Narendra doesn't just want to sue, he wants to hire the Sopranos** to "beat the shit out him" which is the logical conclusion of Lessig's social Darwinist ethics. Of course Zuckerberg could in turn sue Narnedra for damages.

The director David Fincher's Fight Club took a jaundiced-eyed look at late 20th-Century consumer capitalism. The Social Network is a much lighter, if more realistic take on business in the 21st century. He deserves an Oscar.

----------------------

*played by actress Rashida Jones, who dated Obama's longtime speechwriter Jon Favreau (she's single now). A fictional Harvard President Larry Summers has a funny scene. Another co-founder of Facebook, Chris Hughes, helped the Obama Presidential campaign set up its social networking site. And of course Obama went to Harvard Law.

** As the Italian mobster in the Coen brothers' film Miller's Crossing says, "no one's got ethics these days."

(or Lawyer Up!)

[spoiler alert]

I saw "The Social Network" and found it entertaining and thought-provoking, as everyone has been saying. The actors were all good, especially Jesse Eisenberg, Andrew Garfield, and Justin Timberlake.

Basically, Jesse Eisenberg plays Mark Zuckerberg whose Harvard friend Eduardo Saverin, played by Andrew Garfield, gives him a computer algorithm that allows him to create a software program Facemash which gets him noticed by the Winklevi twins and their friend Divya Narendra, who hire him to program their dating program. He uses some of the ideas from their dating program, his Facemash program, and some start-up money from Saverin to start his Facebook site.The ever-more-popular website gets noticed by Justin Timberlake's Sean Parker who lures Zuckerberg out to Silicon Valley and connects him with venture capitalists. And the website becomes more popular. Keep in mind, though, that Saverin did give him the original algorithm and the original start-up money.

Some random thoughts: Facebook caught on because of the aesthetic design which lacked advertisements and the relationship status on people's profiles. It caught on despite the existence of similar websites like MySpace and Friendster, and became a success because of the various efforts of Mark Zuckerberg and his business partners. No one can take that away from them, but the movie does portray Zuckerberg screwing over his friend and business partner Saverin. Saverin was duped into signing away his stake in the company, so I guess the morale of the story is one should have one's own lawyers look over these sorts of contracts even if it involves a contract with a "friend."

The characters seem real because they have both likable and unlikable qualities. They're complicated. Garfield's Saverin was the most sympathetic in the film, although you could see how Zuckerberg could be annoyed by his frequent mentions of his father. Also, the movie seems to say Saverin's focus on advertising was the wrong way to go for Facebook and Zuckerberg was correct to follow the business advice of Timberlake's Parker who among other things connected Zuckerberg with venture capitalists and suggested he change the name of the site from The Facebook to just Facebook. Parker and Zuckerberg also had an endearing desire to "stick it to the Man," or at least to stick to people who were patronizing and disrespectful to them. Maybe it's the adolescent boy in me who finds that trait appealing, because the movie also shows how that trait can lead people astray. Also, Parker and Zuckerberg obviously have other psychological "issues" for all of their business savvy.

The movie posits the possibility that Zuckerberg set up his businesses partners Saverin - via the cruelty to a chicken - and Parker - via a police bust - which really would have been Machiavellian, but ends up suggesting that he probably didn't. One of his lawyers* advises him to settle a lawsuit because a jury might think he had indeed set up his business partners to get them out of the way, because of some unethical and malicious behavior Harvard had disciplined him for before Facebook was up and running.

In my previous post, I had a quote where David Carr and producer Scott Rudin want to divide the views on Zuckerberg into Tragic or Heroic. Why not be dialectical and describe him as both? Or can the Tragic encompass the Heroic? Zuckerberg can be a visionary, perfectionist, tough, driven workaholic who got lucky and still be a flawed, unethical asshole.

Update: In his article on how the movie ignores the importance of "network neutrality," Lawrence Lessig writes

To his credit, Sorkin gives [Zuckerberg] the only lines of true insight in the film: In response to the Winklevi twins' lawsuit, he asks, does "a guy who makes a really good chair owe money to anyone who ever made a chair?" And to his partner who signed away his ownership in Facebook: "You’re gonna blame me because you were the business head of the company and you made a bad business deal with your own company?" Friends who know Zuckerberg say such insight is common. No doubt his handlers are panicked that the film will tarnish the brand. He should listen less to these handlers. As I looked around at the packed theater of teens and twenty-somethings, there was no doubt who was in the right, however geeky and clumsy and sad.My guess is that Carr, Rudin and Lessig can identify with Zuckerberg in that they have screwed over some Saverins of their own on the way to success.

Lessig happens to be a professor at Harvard Law School and the director of the Edmond J. Safra Foundation Center for Ethics. He's right about net neutrality and the chair-making analogy, but I don't see what's ethical about misleading your business partner about what's in the contract he was signing. Saverin wouldn't have signed it had he understood what he was signing. In Lessig's view it's acceptable to screw over a sucker? I realize a lot of businesses operate this way - not to mention whole industries like Wall Street - but is it moral?

Is that good business ethics to lie to your business partners? Evidently it's good business. Marx was right about how capitalism reduces everything to the "cash nexus" which is why America is such a litigious society. At one point the old money Winklevi twins are at odds about suing Zuckerberg over intellectual property theft. One twin doesn't want to sue because "that's not how things are done at Harvard" which is a nod at the old aristocratic traditions and codes of honor, a vestigial feudal frame of reference. The twins' partner Divya Narendra doesn't just want to sue, he wants to hire the Sopranos** to "beat the shit out him" which is the logical conclusion of Lessig's social Darwinist ethics. Of course Zuckerberg could in turn sue Narnedra for damages.

The director David Fincher's Fight Club took a jaundiced-eyed look at late 20th-Century consumer capitalism. The Social Network is a much lighter, if more realistic take on business in the 21st century. He deserves an Oscar.

----------------------

*played by actress Rashida Jones, who dated Obama's longtime speechwriter Jon Favreau (she's single now). A fictional Harvard President Larry Summers has a funny scene. Another co-founder of Facebook, Chris Hughes, helped the Obama Presidential campaign set up its social networking site. And of course Obama went to Harvard Law.

** As the Italian mobster in the Coen brothers' film Miller's Crossing says, "no one's got ethics these days."

Monday, October 04, 2010

I saw the latest episode of Bored to Death, "Make It Quick, Fitzgerald!," on HBO and it was the funniest, best thing I've seen in a while. No joke. Brilliant writing and great performances by Jason Schwartzman, Zach Galifianakis, Ted Danson, Oliver Platt, and the other actors. They looked like they had fun making it.

Plus the script mentions Menticide. Either that or Jason Schwartzman ad libbed.

Plus the script mentions Menticide. Either that or Jason Schwartzman ad libbed.

American Psycho

(or American Idiot*)

David Carr is sampling from the wrong group of young Americans:

18-29 year-olds 57%

65 and older 38%

If young people do not turn out for the mid-terms next month (they historically don't) and Republican retirees do as they historically do - what else do they have going on? - Republicans will take the House.

Onion review of American Psycho.

------------------------

*idiot is taken from the Greek idiotus meaning someone with no interest in politics

(or American Idiot*)

David Carr is sampling from the wrong group of young Americans:

But the movie [The Social Network] could well serve as a referendum on business aggression and ambition that breaks along generational lines.

Many older people will watch the movie, which was No. 1 at the box office last weekend, and see a cautionary tale about a callous young man who betrays friends, partners and principles as he hacks his way to lucre and fame. But many in the generation who grew up in a world that Mr. Zuckerberg helped invent will applaud someone who saw his chance and seized it with both hands, mostly by placing them on the keyboard and coding something that no one else had.

By the younger cohort’s lights, when you make an omelet this big -- half a billion users -- a few eggs are going to get broken. Or as the film’s artful tag line suggests, "You don’t get to 500 million friends without making a few enemies along the way."

"When you talk to people afterward, it was as if they were seeing two different films," said Scott Rudin, one of the producers. "The older audiences see Zuckerberg as a tragic figure who comes out of the film with less of himself than when he went in, while young people see him as completely enhanced, a rock star, who did what he needed to do to protect the thing that he had created."Ezra Klein reflects on the Gallup poll about who likes Obama:

18-29 year-olds 57%

65 and older 38%

If young people do not turn out for the mid-terms next month (they historically don't) and Republican retirees do as they historically do - what else do they have going on? - Republicans will take the House.

Onion review of American Psycho.

------------------------

*idiot is taken from the Greek idiotus meaning someone with no interest in politics

From Sewell Chan's article: camps within the Fed.

- Doves: William C. Dudley, New York Fed; Eric S. Rosengren, Boston Fed, Janet L. Yellen, Fed vice chairwoman (was San Fransisco Fed); (all three have votes on the 2010 FOMC)

- Leaning Dovish: James Bullard, St. Louis Fed; Charles L. Evans, Chicago Fed; Sandra Pianalto, Cleveland Fed; Sarah Bloom Raskin, Fed governor; Daniel K. Tarullo, Fed governor; (four have votes on the 2010 FOMC)

- Middle: Ben S. Bernanke, Fed chairman; Elizabeth A. Duke, Fed governor; Dennis P. Lockhart, Atlanta Fed; (two have votes on the 2010 FOMC)

- Leaning Hawkish: Narayana R. Kocherlakota, Minneapolis Fed, Kevin M. Warsh, Fed governor (Warsh has a vote on the 2010 FOMC)

- Hawks: Thomas M. Hoenig, Kansas City Fed; Richard W. Fisher, Dallas Fed; Jeffrey M. Lacker, Richmond Fed; Charles I. Plosser, Philadelphia Fed (Hoenig has a vote on the 2010 FOMC)

James Hamilton discusses QE2. (via Mark Thoma) Hamilton quotes New York Fed President William Dudley:

some simple calculations based on recent experience suggest that $500 billion of purchases would provide about as much stimulus as a reduction in the federal funds rate of between half a point and three quarters of a point. But this estimate is sensitive to how long market participants expected the Fed to hold on to these assets.

Saturday, October 02, 2010

DeLong posts a quote from Joe Gagnon

Away from the zero bound, monetary policy can stick to buying safe short-term assets because money yields zero and all other assets have a positive yield. At the zero bound, as you note, for monetary policy to have any effect it must buy other types of assets that do not have zero yield. But in both regimes the way monetary policy works is by pushing down the rates of return on financial assets. That is quite distinct from fiscal policy which works by increasing demand directly, albeit at the expense of higher rates of return on financial assets. And of course, helicopter drops increase demand directly without increasing rates of return on financial assets.So maybe QEII isn't a helicopter drop, technically speaking? I don't know, I can't really follow what they're talking about. Is the Fed doing fiscal policy in Gagnon's view? So you push down the rates of return on financial assets and then what happens?

Friday, October 01, 2010

Incoming!

More evidence that the Fed intends to drop QEII on us after the election. Via Mark Thoma who writes:

QEI was the expansion of the Fed's balance sheet from around 800 billion to 2.3 trillion, and QEII would increase the size of the balance sheet even further -- though if they do move to QEII, how much and how fast that balance sheet would be extended is not known.

Wednesday, September 29, 2010

Obama in Rolling Stone:

The idea that we’ve got a lack of enthusiasm in the Democratic base, that people are sitting on their hands complaining, is just irresponsible.... We have to get folks off the sidelines. People need to shake off this lethargy, people need to buck up. Bringing about change is hard -- that’s what I said during the campaign. It has been hard, and we’ve got some lumps to show for it. But if people now want to take their ball and go home, that tells me folks weren’t serious in the first place. If you’re serious, now’s exactly the time that people have to step up.

Simon Johnson on how things could turn quickly for Obama:

What this conventional wisdom misses is that we experienced a severe credit crisis of the kind more typically seen in recent decades in middle-income emerging-market countries. The U.S. can recover quickly -- and jobs can come back much faster than expected -- but only if the dollar now depreciates.

Like it or not, significant dollar depreciation is more probable than most now suppose. The depth of the crisis in late 2008 stunned many U.S. observers, but its features were fairly obvious to people who have worked in Russia, Mexico, Argentina, or South Korea. Similarly, the recovery can share some characteristics with what those countries have experienced.

Korean Rebound

We shouldn’t anticipate any kind of immediate growth miracle in the U.S., but just keep in mind that after its economic collapse in 1997-98, South Korea grew almost 11 percent in 1999, while Russia -- written off in economic terms after its currency, public finances and banking system effectively collapsed in the fall of 1998 -- still managed a 6.4 percent expansion in 1999 and 10 percent in 2000.

The main reason the U.S. isn’t bouncing back so fast is because of exports and the dollar. South Korea, Russia, and other emerging markets that go through severe crises usually undergo a sharp depreciation in the inflation-adjusted value of the currency, making them hypercompetitive, at least for a while. This makes it easier to replace imports with domestic goods and services and much more attractive to export.

In contrast, the global financial crisis actually strengthened the U.S. dollar as it was seen as a haven, although the dollar has fallen somewhat from its recent peak against major trading partners.

.svg.png)

A reciprocity requirement: The easy and legal way to stop currency manipulation by Daniel Gros

Overall it seems that the rest of the world with free capital markets can do little to stop the Central Bank of the People’s Republic of China to continue "steering" its exchange rate by accumulating more and more international reserves - it does not matter whether these are US or Japanese. The US, Japan, or the ECB cannot do the same because China has capital controls and there are simply no significant renminbi assets that foreigners are allowed to invest in.

...

But there is another way. The US (and Japan) could easily prevent the Chinese Central Bank from continuing its intervention policy without breaking any international commitment. The US and Japan only need to invoke the principle of reciprocity and declare that they will limit sales of their public debt henceforth to only include official institutions from countries in which they themselves are allowed to buy and hold public debt. Instead of the "moral suasion", tried in vain by the Japanese, the Chinese authorities would just be told that they can buy more US T-bills Japanese bonds only if they allow foreigners to buy domestic Chinese debt.

Imposing such a "reciprocity" requirement on capital flows would be perfectly legal - although the US (and Japan and all EU member countries) have notified the IMF that they have liberalised capital movements under Article VIII of the IMF. Yet, in contrast to the area of trade, there are no legal constraints on the impositions of capital controls.

This "reciprocity" measure would of course be equivalent to a very specific form of controls on capital inflows. Capital controls are always somewhat leaky, but not in this case because the Chinese Central Bank would find it difficult to hide its huge investments going through western financial institutions. No reputable financial institution would dare to become a hidden intermediary for the Chinese given that no institution bidding for hundreds of billions of T-Bill would take the risk of secretly fronting the Chinese government or central bank as it would have to certify that the beneficial owner is not from a country in which foreigners cannot buy and hold public debt instruments.

As a practical matter the introduction of the reciprocity requirement should provide a grand fathering of the existing stocks of Chinese official assets abroad (already above $2,500 billion). However, the Central Bank of China would still not be able to continue its interventionist policy - and that is what counts for foreign exchange markets.(via Mark Thoma)

China does have capital controls unlike other countries. If the US blocks China and they in turn buy from Japan who has to in turn buy from the US, then we can block Japan also.

It's important to point out that the world economy is working under exceptional circumstances as Krugman continuously points out. There's too much savings and too much unemployment and not enough demand. China and Germany are exacerbating the problems with beggar-thy-neighbor policies.

Stephen Roach argues that China should adopt policies to boost its consumer spending.

China’s gross domestic saving rate is 54 percent of national income, the highest in the world for a major economy. But its consumption share of G.D.P. is only about 36 percent, the lowest for a major economy and about half the 70 percent ratio in the United States.

I would therefore urge China to opt for aggressive and immediate pro-consumption structural policies. Stimulating domestic consumer demand would be a far more direct - and potentially a far less destabilizing - way of reducing saving and trade imbalances than a currency realignment would be.