Krugman seems to be changing his course here, along with expanding on an earlier blog posting about WWII. He used to argue that the Fed needs to create inflation, just what Bernanke used to argue with respect to Japan. Now he says:

Just saying "monetary policy" doesn’t cut it. Yes, the Fed has tools available even though short-term rates are up against the zero lower bound, and it should be using them to the max. But their effect is highly uncertain; I don’t think anyone can count on the Fed to deliver, on cue, Rogoff’s "two or three years of slightly elevated inflation." In fact, the whole logic of the liquidity trap suggests that if central banks can gain any leverage at all, it’s only by credibly committing to inflation over a fairly sustained period.

So how might inflation be achieved? Actually, we have a good example: the end of the Great Depression.

The immediate cause of the depression’s end was, of course, a very large fiscal stimulus, also known as World War II. But why didn’t the US slide back into depression when the war was over? Many people thought it would; the decline of Montgomery Ward had a lot to do with Sewell Avery’s policy of refusing to expand and hoarding cash in preparation for the return of depression.

Why, then, didn’t depression return? The best answer I’ve come up with is that the depression was, at least in part, a Koo-type balance sheet slump -- and the private sector emerged from World War II with much-improved balance sheets.

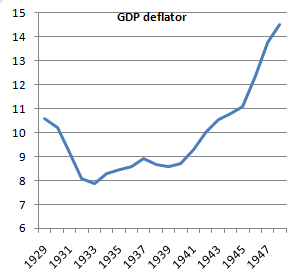

And inflation was an important part of that improvement. Here’s the GDP deflator (a measure of the overall price of things America produces) from 1929 to 1948:

Bureau of Economic Analysis

Prices rose about 70 percent during the buildup to war, the war itself, and the immediate aftermath. This greatly reduced the real value of outstanding debt– the reverse of the debt deflation that took place in the early stages of the depression.

What this example suggests is that yes, inflation can be helpful in getting out of a prolonged slump -- but that getting that inflation probably requires a combination of loose monetary policy with strong fiscal stimulus.

... During WWII we saw something like a 35 percent of GDP rise in government spending; this led to a big rise in GDP.Emphasis added.

No comments:

Post a Comment