Below I sketched out the gist of the arguments made by Robin Wells and Paul Krugman* in their piece

The Slump Goes On: Why? as I understood it.

What's great about their article is that they confront some widely-held misperceptions on what has occurred and what's happening now.

Ostensibly, the piece is a book review of three books: Rajan's

Fault Lines; Roubini and Mihm's

Crisis Economics; and Koo's

The Holy Grail of Macroeconomics.

Wells and Krugman are extremely dismissive of Rajan and argue he's just peddling conservative propaganda. Rajan believes that the Fed held rates too low in the past decade and Roubini and Mihm give this view qualified support. However as Wells and Krugman point out, the Fed was facing possible deflation after the tech stock crash when it lowered rates from 6.5 percent in 2000 to just 1 percent in 2003. Inflation had been at a thirty-five year low and Japan's lost decade was on people's minds at the time.

Rajan blames Democrats, the Community Reinvestment Act and Fannie and Freddie for the subprime crisis. Wells and Krugman say Roubini correctly points out how Rajan is wrong in that the huge growth in the subprime market was primarily underwritten by private mortgage lenders like Countrywide Financial.

Wells and Krugman say Roubini and Mihm give a good overview of Hyman Minsky's highly relevant work and that

Crisis Economics "is a very good primer on how finance gone bad can wreck an otherwise healthy economy." The book makes the essential point that bubbles are not uncommon. "Bubbles have happened in small economies and large, in individual nations and in the global economy as a whole, in periods of heavy public intervention and in eras of minimal government."

Koo's book focuses on the problems economies face in the aftermath of a "Minsky moment" (although he doesn't use that term or mention Minsky). Basically, there is a problem of red ink and deleveraging. Koo focuses on Japan whose nonfinancial corporations were saddled with debt after the real estate bubble burst in the late 1980s. Currently it is households who are deleveraging in America, not corporations.

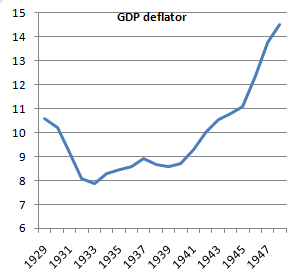

In a blog post Krugman argues that after the Great Depression, World War II inflated away much of the debt.

It will be interesting to see what Wells and Krugman argue in their second article.

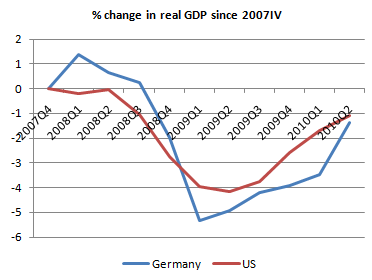

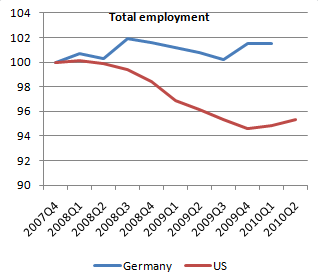

The current slow growth in GDP is reminiscent of the recoveries after the recessions of 1991 and 2001.

However, "only once since World War

II has the unemployment rate stood this high on Labor Day -- during the steep recession of 1982 under President Reagan. It has remained at 9 percent or higher for 16 straight months and is likely to surpass the 19-month record of such high rates set in 1982 and 1983."

The 1982 recession was caused in part by Fed Chairman Volcker jacking interest rates and it was ended by Volcker lowering rates once inflation was tamed. We went into the 2008-2009 recession with rates already low, whereas from 2000-2003 the Fed had room to lower rates from 6.5 to 1 percent.

Bernanke says the Fed has more tools to use if there's a double dip, but apparently these tools aren't worth using to maintain low unemployment. Instead we just get pathetic excuses about structural changes in the job market and the fact that "central bankers alone can't solve the world's economic problems." No, but the Fed's only missions are price stability and maintaining low unemployment and currently it's failing at both.